The ETF Portfolio Strategist: 9 June 2021

Trend Watch

Real estate is running hot lately. Just in time for the start of summer. Deciding why property shares are blowing away most other slices of the major asset classes is a slippery affair, but there’s no debate about the performance sizzle.

Vanguard Real Estate (VNQ), a portfolio of US real estate investment trusts (REITs), continues to trade higher this week, ending today’s session at another record high (June 9). Barring a sharp reversal over the next two days, VNQ is set to post its fourth straight weekly gain.

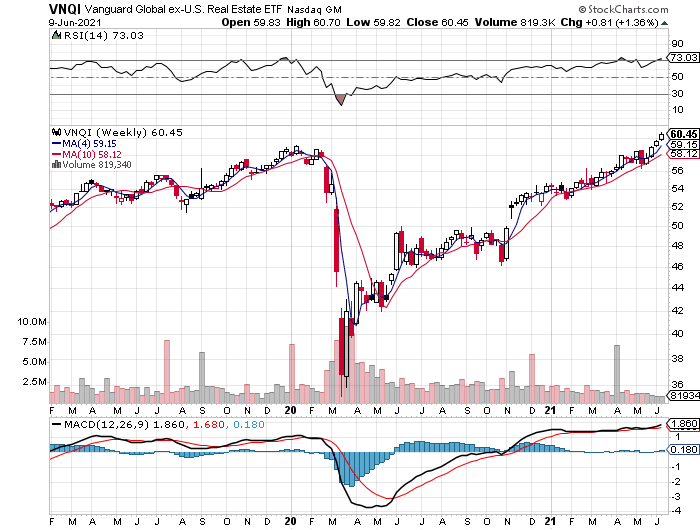

Foreign property/REIT shares are posting similarly strong performance via Vanguard Global ex-US Real Estate (VNQI).

What’s filling the sails of real estate shares? It doesn’t hurt that the recent rise in interest rates has reversed course. After months of trending higher, the 10-year Treasury yield hit a ceiling a few months ago and recently started edging lower. In today’s session, the 10-year rate fell to 1.50% (based on daily data via Treasury.gov) — the lowest in more than three months.

Lower yields on “risk-free” Treasuries is a plus for yield-oriented REITs, which are prized by investors for relatively high payouts rates.

Another narrative that’s making the rounds: as the global economy rebounds, industrial properties are in high demand as the supply-chain network fires up again after the pandemic. “It seems investors are using real-estate ETFs as a means of capitalizing on global logistics concerns,” observes Bloomberg Intelligence ETF analyst Athanasios Psarofagis

The Bloomberg article also notes:

21% of Vanguard’s VNQ are in four stocks: American Tower Corp., Prologis Inc., Crown Castle International Corp. and Equinix Inc. The companies specialize in data storage, wireless infrastructure and warehouses. Exposure to these stocks would suggest investors are taking a bet on storage and supply chain concerns.

Whatever the catalysts, flows into VNQ and related funds have been strong. Last month, for example, VNQ reported inflows of $1.2 billion — its best month in more than two years.

Although the recent decline in the 10-year yield suggests that the bond market has fully priced in the risk of hotter inflation, there’s still a raging debate about how much risk of unexpected pricing pressure lurks. But REITs may be a hedge on higher inflation too, some analysts explain.

“One of the reasons for their recent relatively stable performance might be explained by the cause for the rising bond yields and changing weights structure of the listed real estate sector,” according to FTSE Russell. “Higher inflation expectations are particularly supportive of residential real estate prices. We have witnessed recently that residential is one of the best performing components of listed real estate.”

Considering the broad range of narratives that seem to rationalize higher prices for REITs suggests that this asset class is poised to shine whether inflation heats up or proves to be transitory. That may be assuming too much, but for now the crowd’s buying first and asking questions later on matters of securitized real estate. ■