The ETF Portfolio Strategist: 22 Jan 2023

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

And now for something different: Foreign stocks are offsetting weakness in US assets, which in turn is keeping the potential for a rebound bubbling in our global 16-fund opportunity set (G.B16).

As noted last week, the broad trend appears to be turning from a negative to positive bias. These are still early days, but the tide may be shifting after nearly a year of a broad-based run of bearish bias.

The G.B16 Index continued to push further above its 200-day average, which suggests that the bulls are emerging from their slumber via the perspective of a multi-asset-class portfolio. Although I remain cautious, the case for a bullish outlook will strengthen if G.B16’s 50-day average can rise above its 200-day average and hold on to the trend shift. We’re not there yet, but if markets can rise further over the next several weeks a stronger, clearer upside tipping point is near.

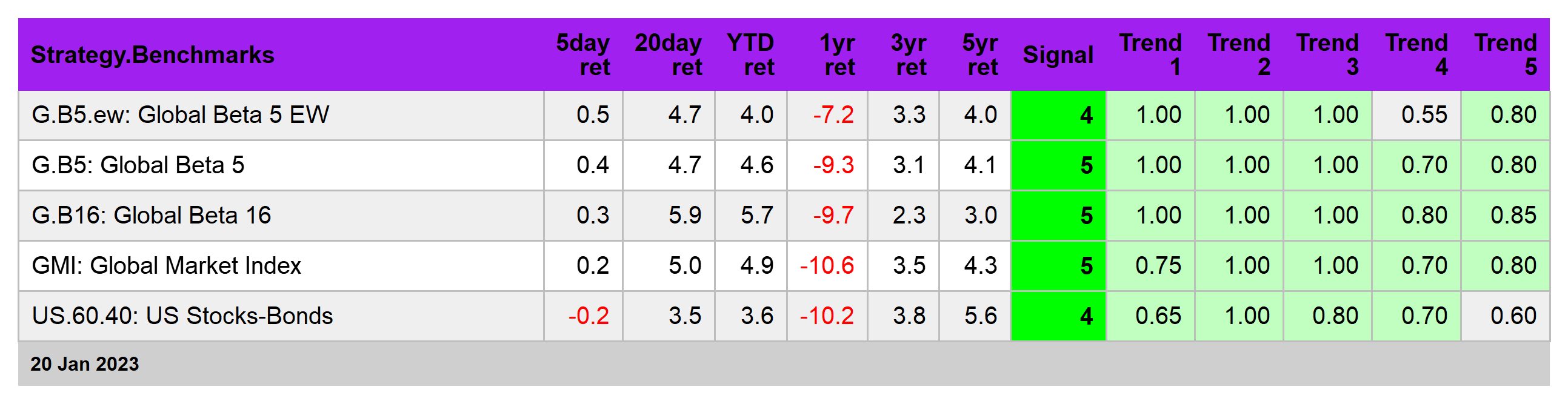

Note that G.B16’s gain over the trailing 5-day window was fueled solely by markets ex-US. The case for international diversification, in other words, appears to be reviving after an extended lull. For details on the metrics in the table below, see this summary. (Note: due to the US holiday on Jan. 15, last week was a four-day trading week in America and so the 5-day return in the table below differs from the calendar-week results.)

Consider, for instance, the 2.3% 5-day rally in Asia ex-Japan equities (AAXJ). That’s the second-best return for that time window. Meanwhile, the ETF’s weekly chart action suggests that this slice of global equity markets is shrugging off its bear-market bias.

There are still plenty of reasons to remain cautious, including the mystery on how much higher the Federal Reserve will lift interest rates and how long it will keep rates relatively lofty. The good news: the next rate hike is expected to slow to a 25-basis-points increase, which would be the softest rise so far. Fed funds futures are pricing in a near certainty for this outlook.

Encouraging, but it’s not yet obvious that this will mark the end of the Fed’s tightening cycle. Even if the hiking is about to end at the Feb. 1 FOMC meeting, analysts are debating how long the rate hikes will last before we see cuts.

All of this leads to the main question: How much of the lag effects tied to monetary policy are already priced into markets? The crowd seems to be betting that the worst of the macro headwinds linked to rate hikes has passed and it’s all smooth(er) sailing from here. The Fed, by contrast, is still inclined to disabuse markets of thinking too far ahead on that score.

Fed Governor Lael Brainard played the tough gal on this point last week, advising that she expects interest rates to stay high despite progress on taming inflation. “Even with the recent moderation, inflation remains high, and policy will need to be sufficiently restrictive for some time to make sure inflation returns to 2% on a sustained basis,” she outlined in a speech.

Markets, however, are more inclined to bet that she and her colleagues will blink. If not, the optimism that’s bubbling in the broad sweep of global markets could fade faster than a snowflake in San Diego. ■

See this summary for design details on the benchmarks.