The ETF Portfolio Strategist: 22 JUNE 2025

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Are markets too complacent about the risks festering around the world? Your editor falls into the camp that responds with an emphatic “yes.” But markets don’t care what your editor thinks.

Following the US attack on Iran yesterday, market tranquility will be tested anew in the days ahead as the crowd attempts to price in what US Secretary of Defense Donald Rumsfeld famously described as the “known unknowns” and, more ominously, the “unknown unknowns.”

What we do know is that the US is describing its military strike on Iran’s nuclear sites as a "spectacular success," President Trump said last night. Pentagon officials this morning said the Iran’s nuclear sites suffered “severe damage.”

What comes next — for geopolitical risk, the global economy and financial markets — is another question altogether. At issue is the pressing question: What could be brewing for second-, third- and fourth-order effects. This is a guessing game, with high stakes and a wide array of possible/plausible scenarios, ranging from bullish to bearish and a substantial range of gray-zone outcomes.

The key variables to monitor that could play key roles for the path ahead include:

Will Iran attempt to close the Strait of Hormuz, a critical oil transit chokepoint in the Persian Gulf. Reports this morning advise that Iran’s parliament backed a measure to close this key shipping route. It could be bluster, but in the current climate it’s too early to dismiss.

Will Russia and China react? If so, how? Both countries have become closely aligned with Iran recently and the loss of a key ally could trigger some response by Moscow and/or Beijing. Russia has already lost a key Middle East ally with the overthrow of the Assad regime in Syria and so the prospect of regime change in Iran could motivate a reaction. Iran’s foreign minister is reportedly heading to Russia to meet with Russian President Vladimir Putin following the US strikes. Meanwhile, former Russian President Dmitry Medvedev, who’s the deputy chairman of the Security Council of Russia, today said that Trump "has pushed the US into another war" and so countries are "ready to directly supply Iran with their own nuclear warheads."

Two proxies for monitoring sentiment that are on my short list:

Crude oil — prices are up substantially since Israel launched its first attack on Iran more than a week ago. Will prices continue to rise? If so, for how long? At stake is the directional bias for headline inflation and the implications for monetary policy — at a time when the Federal Reserve is already wary of future inflation risk re: tariffs.

A related risk gauge: guesstimates via betting markets on whether Iran will close the Strait of Hormuz. Earlier today, the pricing reflected a ~52% chance, but that’s since pulled back to 36% as we write, based on data from Polymarket.

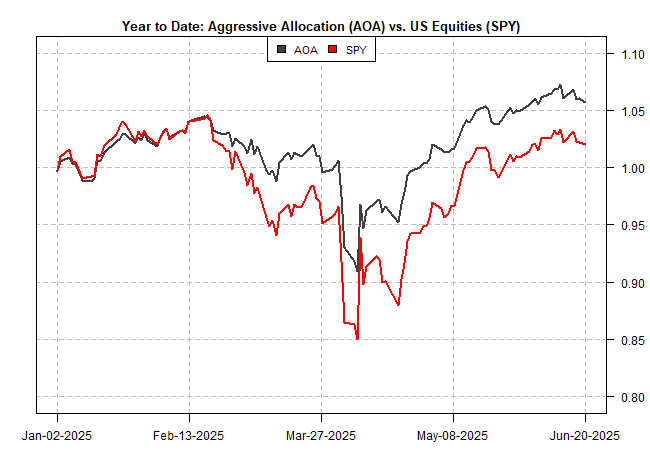

As for market action last week (which may be ancient history at this point), the crowd more or less yawned from a global asset allocation perspective. Our four proxy funds edged lower, but year to date a clear upside bias rolls on. The losses from the April tariff-induced selling have been recovered, and then some, and the trend signals remain risk-on across the board.

Note that all four global asset ETFs are still outperforming US stocks (SPY) so far this year. I expect that will continue, although perhaps in a more volatile market environment. But as I’ve been noting for months, return forecasts have remained favorable for global diversification and the current spike in geopolitical risk doesn’t offer a compelling reason to think otherwise.

Choosing between markets is a bit challenging at the moment, in part because the trend profiles are now mostly positive in nearly every corner.

The key question for the week ahead: How will the trend analysis evolve in the wake of the Iran attack? This could turn out to be a fast-moving, highly fluid situation. There are a lot of moving parts to this analysis and so your editor remains humble in the extreme on trying to forecast where we’re headed. Meantime, it remains to be seen if markets can shrug off one more non-trivial risk factor.

Whatever the answer, the week ahead looks set to be eventful, for one reason or another. Meanwhile, global diversification still looks like the worst option… except when compared with everything else. ■

Hi James, I really like your article! It certainly made me think, so, 2 comments [1] about that retired Russian leader saying "other countries" will/might give Iran nuclear warheads" probably needs more thought. Such as - Who are these "other countries?" Its a very short list, and I don't think any of the big powers would want to start a nuclear war. And [2] I asked my AI tool to research war periods and market returns over the past 200 years for UK, Holland, US and Japan, and it came up with this: in 100% of situations tested, the markets initially has high volatility and a drawdown but after a period of adjustment, carried on with no further major drawdowns.