The ETF Portfolio Strategist: 23 September 2020

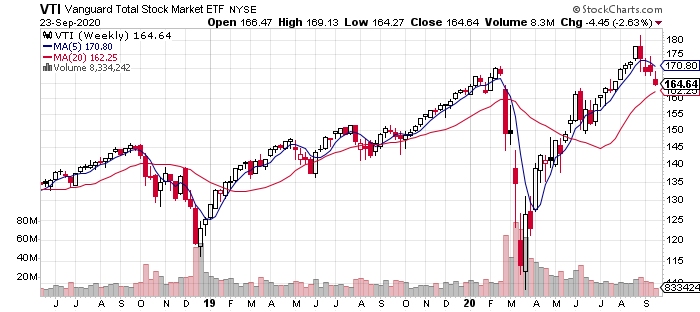

US Stocks Flirting With Fourth Weekly Decline: It’s only Wednesday, Sep. 23, but the downside bias for US equities is building. At today’s close, Vanguard Total US Stock Market (VTI) shed 2.6% for the week so far. Today’s sharp pullback more than reverses two days of moderate gains and so it doesn’t take a raging bear to imagine that VTI is flirting with its first run of four straight weekly declines in more than a year.

The US bond market isn’t doing much better. There’s been a lot of chatter lately about the decline and fall of bonds as reliable diversification tools and recent results play into that narrative. For example, the investment-grade US fixed-income benchmark via Vanguard Total US Bond Market (BND) slipped to its lowest close in nearly a month today and is off fractionally for the week so far. Amid the latest market setbacks, bonds aren’t providing much ballast for weakness in share prices.

There’s not much upside in other asset classes either. From commodities (GCC) to real estate investment trusts (VNQ) to foreign shares (VEA and VWO) and beyond, it’s hard to find gainers lately.

A conspicuous exception: the US dollar. For investors who treat the greenback as an asset class, this week to date has been a gift: Invesco DB US Dollar Index Bullish Fund (UUP) is up 1.6% since Friday’s close. The catalyst, in part: commentary this week by the Chicago Fed President, who said the Federal Reserve may begin raising rates before inflation averages 2%. The forex market interpreted the remark as a pullback from the dovish average inflation targeting policy the central bank rolled out recently. It remains to be seen if the revival of a bullish-dollar aura persists, but for now UUP (which tracks a basket of major foreign currencies in dollar terms) has reversed its months-long slide.

Risk-Off Is Looking Increasingly Timely: The latest round of market weakness may be noise, but the gradually expanding risk-off signals for Global Managed Drawdown (G.B16.MDD) continues to look savvy. (For details on the strategy rules for the proprietary and benchmark portfolios, along with information on the risk and return metrics in the tables below, see this summary.)

At the end of last week, five of the 16 funds in G.B16.MDD were in a risk-off posture and there may be new arrivals when we run fresh numbers after the close this Friday. Risk management isn’t flawless, however, and G.B16.MDD is getting pinched lately, as are the two other proprietary strategies, per the table below.

But compared with the passive benchmark – Global Beta 16 (G.B16), G.B16.MDD and Global Managed Volatility (G.B16.MVOL) — risk management continues to enjoy a strong performance edge so far this year. (Note that the three proprietary strategies listed above hold the same funds as the benchmark (G.B16) – the only difference is the risk-management overlay.)

Meanwhile, Global Managed Volatility (G.B16.MDD) is still risk-on across these 16 funds. Until the current rebound in volatility on a trailing 10-day basis rises above the 99th percentile over the previous 100 days, the strategy remains in offensive mode. But market conditions have changed and if higher vol persists G.B16.MDD will soon start shifting to risk-off.

Global Minimum Volatility (G.B16.MINV) is lagging this year, but that’s (partly) by design since a smooth ride is the goal, albeit with an attempt to maximize returns as much as possible. It’ll be interesting to see how G.B16.MINV fares if we’re heading into a new volatility storm.

Here’s how our three home-grown risk-managed strategies stack up this year against the benchmark:

Finally, here’s BlackRock’s quartet of asset allocation funds targeting several flavors of risk.

Note that the current round of market weakness is starting to bite into the most aggressive of these funds via iShares Aggressive (AOA), which is showing a bit of blood for the year-to-date results. ■